How to File a Water Damage Insurance Claim in Spartanburg County

Filing a water damage insurance claim in Spartanburg County feels overwhelming when you’re also dealing with standing water in your home. The documentation requirements, adjuster coordination, and policy language interpretation all compete for attention at a moment when you just want someone to fix the damage. This step-by-step guide covers the complete claim filing process for Spartanburg County homeowners — what to do in the first hour, what documentation you need, and how to work with your adjuster to maximize your recovery.

In this post, we cover the claim process timeline, what documentation drives the best outcomes, how to handle common disputes, and how a professional restoration company can make the entire process significantly smoother.

Filing a Water Damage Claim in Spartanburg County?

We handle documentation and adjuster coordination from day one. Call (888) 376-0955 for immediate assessment and claim support.

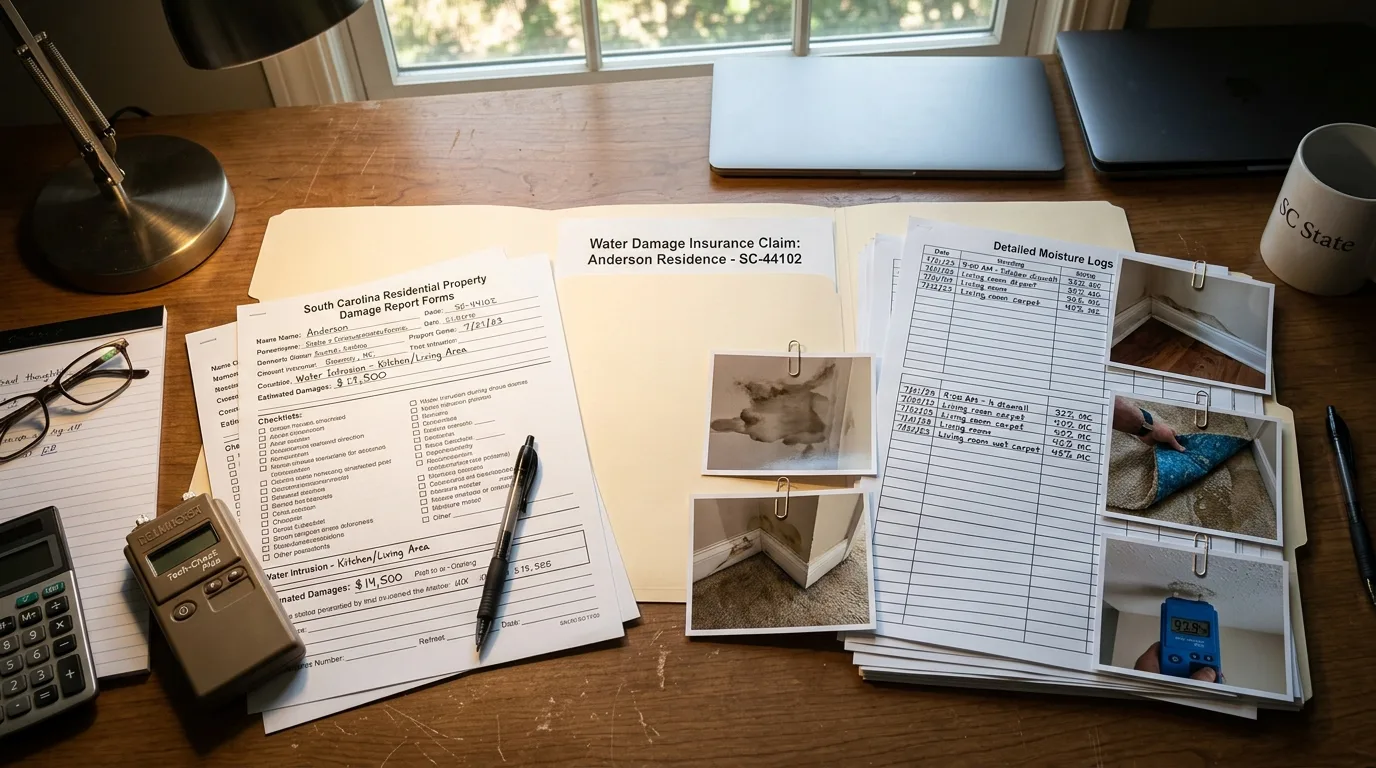

Step 1: Document Before You Touch Anything

The single most important thing a Spartanburg homeowner can do in the first minutes after discovering water damage is document the scene before any cleanup begins. This documentation establishes the original condition of the loss — the baseline that your entire claim is built on.

What to photograph and video:

- Every affected room from multiple angles — wide shots showing the full room context and close-ups of specific damage

- The water source if visible — the failed pipe, the roof penetration, the overflowing appliance

- Water levels on walls (mark the waterline if visible with tape before it dries)

- Damaged personal property in place before it is moved

- Time and date stamp on all photos (use your phone’s native camera app which automatically records metadata)

Do not start cleanup before documenting. Moving furniture, removing wet carpet, or starting fans before photographing can create disputes with adjusters about the original extent of the damage.

Step 2: Stop the Water Source

After documenting the scene, stop the water source if it is still active:

- Burst pipe: Shut off the main water supply to the house — typically at the meter or at a main shutoff near the water heater. Know this location in advance; searching for it while the house is flooding wastes critical time.

- Appliance failure: Shut off the supply line to the appliance directly, or use the main shutoff.

- Roof breach: There is typically nothing a homeowner can safely do to stop active roof intrusion — the priority is protecting belongings below and documenting the damage.

- HVAC condensate: Shut off the air handler at the thermostat or circuit breaker.

Step 3: Call for Emergency Response

Call your water damage restoration team immediately — in Spartanburg County, the 24–48 hour mold window means professional extraction and drying equipment should be on-site the same day as the loss whenever possible. Our emergency line — (888) 376-0955 — dispatches immediately, any time.

Then call your insurance company. Most policies require “prompt notification” of losses. What constitutes prompt varies by policy, but calling within the same day is strongly advisable. Have your policy number available. During the call:

- Report the loss and describe the cause

- Ask for your claim number

- Ask what documentation your insurer requires

- Ask when the adjuster will contact you

Do not wait until you’ve assessed the full scope before calling — call when you discover the loss.

Step 4: Understand What Is and Isn’t Covered

Standard homeowners insurance in South Carolina covers sudden and accidental water damage. Review your policy’s water damage exclusions before the adjuster visit:

- Gradual leaks are frequently excluded — document evidence that supports the “sudden” nature of your loss

- Flood damage from external water requires separate flood insurance — not covered by standard policies

- Sewage backup requires a specific endorsement

- Mold sub-limits may cap coverage for mold remediation even when the underlying water event is covered

Our guide on homeowners insurance and water damage in South Carolina covers these exclusions in detail. Understanding your coverage before the adjuster visit allows you to ask the right questions.

Spartanburg County Water Damage Claim Support

Complete documentation, adjuster coordination, and 60-minute emergency response. Call (888) 376-0955.

Step 5: Work With Your Adjuster

Your insurer will schedule an adjuster visit, typically within a few days of the claim filing. For Spartanburg County homeowners, the adjuster will assess the scope of loss, review your documentation, and develop the insurer’s position on coverage and scope.

What helps at the adjuster visit:

- Your own photo and video documentation of the original loss

- The professional restoration company’s scope-of-loss report and moisture documentation

- Any receipts or estimates for damaged personal property

- Copies of prior inspection or maintenance records that support the “sudden” nature of the loss

What a professional restoration company provides for adjusters:

- Moisture logs with daily readings at all documented points

- Thermal imaging showing the full extent of hidden moisture at discovery

- Photo documentation organized by date and location

- Scope of loss report in the format adjusters use

- Direct availability to speak with the adjuster to answer technical questions

This documentation is why engaging a professional restoration company from the first day of the loss produces better claim outcomes than DIY cleanup — the documentation generated by a professional is far more comprehensive and insurer-friendly than what homeowners typically produce on their own.

Step 6: Review the Estimate and Negotiate if Needed

The insurer will produce a claim estimate based on the adjuster’s findings. Review this estimate carefully:

- Does it include all affected materials and areas documented in the restoration company’s scope?

- Does it use current replacement cost pricing for your area (Spartanburg County pricing for drywall, flooring, labor)?

- Does it account for the full structural drying scope, not just the most visible damage?

If the estimate is lower than expected, work with your restoration company to provide supplemental documentation supporting the higher scope. Most restoration companies have experience identifying discrepancies in adjuster estimates and can prepare supplements with the documentation needed to support additional coverage.

Step 7: Avoid These Common Claim Mistakes

Accepting the first estimate without review: Adjuster estimates are starting points, not final settlements. Supplemental claims are normal and expected in complex losses.

Signing a general release before reconstruction is complete: Some insurers press for final settlement before reconstruction is finished. Avoid signing anything that precludes additional claims until you’re confident the full scope has been addressed.

DIY cleanup that removes evidence: Any cleanup done before documentation is complete potentially undermines your claim. This includes pulling wet carpet, painting over damage, or moving damaged items without photographing them in place first.

Delaying professional response: In Spartanburg County’s summer humidity, every day of delay increases mold scope and claim complexity. Delaying professional response while waiting to confirm insurance coverage typically costs more in the end than a same-day response that generates complete documentation.

Frequently Asked Questions

How long does a water damage insurance claim take in Spartanburg County?

Simple, well-documented claims are typically resolved within 2–4 weeks of filing. Complex claims involving mold, structural damage, or coverage disputes can take 4–8 weeks or more. Working with a restoration company that provides complete documentation from day one is the single most effective way to speed claim resolution.

Can my insurer deny a water damage claim in Spartanburg?

Yes — the most common denial reasons are the gradual leak exclusion (the damage developed slowly rather than suddenly), the flood exclusion (external water rather than a plumbing or appliance failure), and inadequate documentation. If a claim is denied, request the specific basis for the denial in writing and consult with a public adjuster if the amount at stake justifies it.

Should I hire a public adjuster for my Spartanburg water damage claim?

Public adjusters represent the homeowner rather than the insurer and typically take a percentage of the settled claim. They may be worth engaging for very large or disputed claims where the difference between the insurer’s estimate and the actual scope is significant. For most standard residential claims in Spartanburg County, a professional restoration company that provides complete documentation and works directly with the insurer achieves similar results without the public adjuster fee.

Water Damage Claim Help for Spartanburg County Homeowners

We document, coordinate with your adjuster, and ensure the full scope of your loss is captured. Call (888) 376-0955.

Related resources: